{kind=link}

Every major oil shock has left a mark on India, sometimes through inflation, sometimes through foreign exchange pressure, and occasionally through wider economic change. The country’s 1991 balance-of-payments crisis unfolded against a backdrop of rising oil prices. High crude costs later pushed difficult conversations around subsidies, fuel deregulation and energy security. More recently, shifts in global supply chains have altered how India buys oil and manages risks.An oil shock is a sudden and significant movement in oil prices, whether upward or downward, that disrupts economic stability. Although the term is typically associated with sharp price increases, steep declines are also considered oil shocks as both can impact inflation, government finances, trade balances, and overall economic growth.The reckoning in 2026 is triggered by what the International Energy Agency described as a collapse of Strait of Hormuz tanker loadings from more than 20 million barrels per day in February to around 3.8 million barrels by early April, and North Sea Dated price that touched $144 a barrel. In some ways the oil shock reminds of 1973. The numbers are different. The architecture of absorption has changed. The underlying dependency has deepened as India imports around 90% of the oil for its consumption.In 2025, an RBI paper highlighted that 10 per cent rise in crude feeds roughly 20 basis points onto headline CPI. How have global oil shocks repeatedly reshaped India’s economy? In this story we trace the country’s journey through five decades of major crude disruptions –from the 1973 Arab embargo to the latest Hormuz crisis and try to understand how each shock influenced economy and policy decisions, while tracking the evolution of India’s response over time.

1973-74: The Arab oil embargo

In October 1973, Arab members of OPEC imposed an embargo on countries that had supported Israel in the Yom Kippur War. Crude prices moved from roughly $3 a barrel to $12 by early 1974. The Economic Survey of India 1974-75 recorded that the petroleum import bill surged that year, contributing to higher wholesale price inflation. India was then importing approximately 30 per cent of its petroleum needs under a government-administered pricing system.The then Finance Minister Y.B. Chavan told Parliament that the cost of oil imports would have “profound implications” for India. Agriculture Minister Fakhruddin Ali Ahmed warned that food production had been disrupted by the energy crisis as India faced serious drought this year. Kerosene rationing began in New Delhi on February 1, 1974. In some cities, including Bangalore, kerosene was sold at police stations following civil unrest.

1979-80: The Iranian revolution

The Iranian Revolution of February 1979 removed the world’s second-largest oil exporter from the market within weeks. Crude prices climbed from around $14 a barrel in early 1978 to $39 by 1980. The Economic Survey of India 1979-80 records that the petroleum import bill rose steeply as a share of both merchandise exports and GDP. “The balance of payments came under severe pressure during 1979-80 because of the sharp increase in crude oil prices and prices of other imports and a large volume of imports necessitated by domestic shortages. The very same domestic constraints also depressed exports. As a result the trade gap widened to Rs. 2233 crores in 1979-80 as compared with Rs. 1088 crores in 1978-79. Foreign exchange reserves (excluding gold and SDRs) declined by Rs. 56 crores during the year whereas they had risen continuously and substantially in previous years.” the survey noted. India subsequently approached the International Monetary Fund and entered an SDR 3.9 billion Extended Fund Facility in 1981-82, partly due to cumulative balance-of-payments pressure from two successive shocks. 1990-91: The Gulf warIraq’s invasion of Kuwait in August 1990 pushed Brent crude prices within weeks. The crisis struck an economy that was already under pressure from widening external imbalances built up through the 1980s. According to the World Bank’s India Country Economic Memorandum, 1991 (Report No. 9412-IN), India’s current account deficit rose from 1.7 per cent of GDP in 1980–81 to 3.1 per cent in 1989–90, while external debt increased from $20.6 billion to $63.1 billion during the same period. The report also noted that the debt-service ratio had climbed sharply from 9.3 per cent of gross current receipts in 1980–81 to above 27 per cent by the late 1980s, leaving the economy increasingly vulnerable to external disruptions.The World Bank noted that stress had begun building even before the Gulf crisis intensified. “The balance of payments came under increasing strain even before the Gulf crisis because of a slowdown in export growth to hard currency areas and growing difficulties in arranging commercial borrowing,” the report said. It added that foreign exchange reserves had “fallen to 7 weeks of imports by end-July 1990”, while major international rating agencies had already begun reviewing India’s credit profile. The report framed the situation describing oil shock as one of the triggers, noting “Higher oil prices thus hit the Indian economy when it was already on the verge of a foreign exchange liquidity crisis.”“The oil shock resulting from developments in the Persian Gulf precipitated an economic crisis in India. The shock itself was not as severe as those of 1973-74 or 1979-80, but it came after years of fiscal and balance of payments deficits that had greatly weakened the economy and eroded foreign confidence” the report noted describing the Gulf war situation in India. According to the World Bank, “the additional import costs of higher oil prices for 1990/91… was about $1050 million, equal to 0.4% of GDP and 4.6% of exports of goods and services.” The institution also estimated that “India’s overall terms of trade declined by 4% in 1990/91, equivalent to a loss of 0.7% of GDP,” while “loss of remittances and other factors added about $870 million to foreign exchange costs.”The government pledged 47 tonnes of gold with the Bank of England and the Union Bank of Switzerland as collateral for emergency external borrowing. IMF records show India drew on a Stand-By Arrangement (SDR 2.2 billion) and a Compensatory Financing Facility (SDR 1.4 billion) in 1991-93. The Economic Survey 1991-92 placed the current account deficit at $9.7 billion, or 3.1 per cent of GDP.Presenting that year’s budget, the then Finance minister Manmohan Singh said: “There is no time to lose. Neither the Government nor the economy can live beyond its means year after year. The room for manoeuvre, to live on borrowed money or time, does not exist any more.” The New Economic Policy announced in July 1991 — covering industrial delicensing, tariff rationalisation, and partial rupee convertibility — was partly a conditionality attached to IMF support.

2007-08: Crude at $147

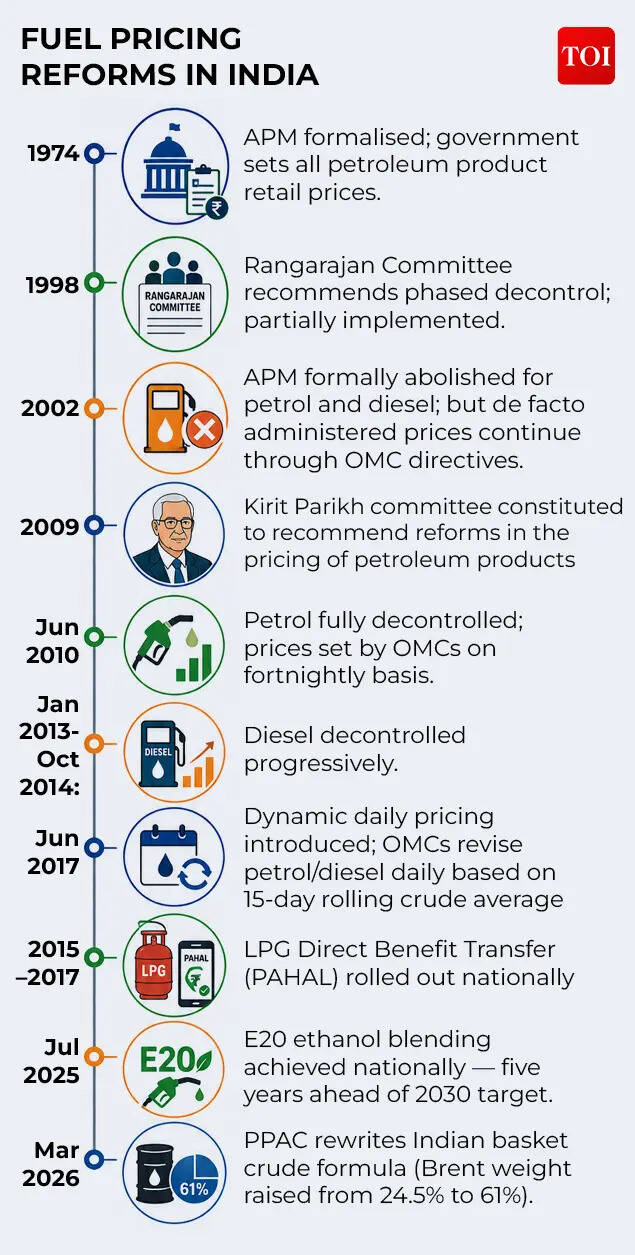

The commodity price cycle of 2007-08 pushed Brent crude to an intra-day high of $147.50 on July 11, 2008, a level not exceeded for nearly two decades. Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum collectively accumulated under-recoveries exceeding Rs 1 lakh crore in FY09. The government issued oil bonds to partially compensate, shifting the liability forward rather than booking it immediately.When international crude prices touched an all-time high of “$142 per barrel in July, 2008”, the government said it did not fully pass the increase on to consumers. In a 2010 statement, then Petroleum Minister Murli Deora said the government and public sector oil companies had together absorbed “under recoveries of more than Rs 1 lakh crore.” He also said fuel prices were rolled back in December 2008 and January 2009 after global crude prices eased. According to the statement, petrol prices stood at Rs 47.51 per litre in June 2006 and Rs 47.93 per litre on June 24, 2010, just before petrol price deregulation. Despite the price revisions, Deora said “there will still be the under recovery of Rs 53,000 crore which the Government and OMCs will have to bear during 2010-11.”

The Kirit Parikh Committee, constituted in 2009 to address the administered pricing system, reported in February 2010. “At the same time 2008 saw an unprecedented rise in oil price on the world market…Given our increasing dependence on imports, domestic prices of petroleum products have to reflect the international prices.” The Parikh committee recommended. Later, petrol prices were deregulated in June 2010, the first structural change to India’s retail fuel pricing architecture since the APM’s introduction.

2011-14: Three years above $100

The Arab Spring of 2011 reduced Libyan oil output and sustained Brent above $100 a barrel for most of the period from 2011 to 2014. RBI Balance of Payments data shows the current account deficit widened to 4.8 per cent of GDP in Q3 of FY2012-13, with petroleum imports a primary driver. Diesel prices were deregulated in October 2014, after crude prices had already begun falling. In these years, the rupee also came under strain from the Eurozone debt crisis, capital outflows and widening domestic deficits. After starting 2011 at around 44.76 against the dollar, the currency slid to 54.30 by December. The stress peaked during the 2013 “taper tantrum”, when expectations of tighter US monetary policy triggered capital flight from emerging markets and pushed the rupee to a then-record low of 68.85 per dollar in August 2013.

2020: Covid and the price collapse

The COVID-19 pandemic produced a fall rather than a rise in crude prices. WTI crude futures traded at minus $37.63 a barrel on April 20, 2020, as demand collapsed and storage filled. India’s crude basket averaged around $20-25 a barrel in April 2020. However, the sharp fall in crude prices during the pandemic was followed by a reversal as economic activity resumed globally. As demand recovered and energy markets tightened, international crude prices moved higher, leading to an increase in domestic fuel prices, though policy interventions continued to cushion the impact. In a December 2022 statement, Petroleum minister Hardeep Singh Puri told Parliament that while the average price of India’s crude basket had increased by 102 per cent — from $43.34 in November 2020 to $87.55 in November 2022– “the retail prices of Petrol and Diesel have increased in India by only 18.95% and 26.5%” during the same period. He also said, “Prices of Petrol and Diesel have not been increased by public sector OMCs since 6th April 2022, despite record high international prices.“ The government said it had reduced central excise duty twice, resulting in a cumulative reduction of Rs 13 per litre for petrol and Rs 16 per litre for diesel, which was “fully passed on to consumers”. The statement also highlighted the cost of the intervention, noting that the three public sector oil retailers – IOCL, BPCL and HPCL–had moved from a combined profit before tax of Rs 28,360 crore in the first half of FY22 to a combined loss of Rs 27,276 crore in the first half of FY23.

2022-23: Russia’s invasion and the sourcing shift

Russia’s invasion of Ukraine on February 24, 2022 led to a significant change in India’s crude oil sourcing. Before the invasion, Russia accounted for roughly 2 per cent of India’s crude imports. The G7 price cap on Russian oil, effective from December 2022, created a discount — Urals crude traded $15-20 below Brent at its widest — that Indian refiners, as non-G7 entities, were not barred from using. Russia’s share of Indian crude imports rose to 21.6 per cent in FY23, 35.9 per cent in FY24, and 35.8 per cent in FY25, according to official trade data. India’s crude import bill fell to $132.4 billion in FY24 from $157.5 billion in FY23, partly reflecting the discounted Russian volumes.US secondary sanctions in November 2025 targeted Russian companies–Rosneft and Lukoil. Cargo tracking data from Kpler showed Russia’s share in India’s total crude imports fell below 25 per cent between December 2025 and February 2026, the first time in two years.

2025-26: The Hormuz disruption

The IEA’s Oil Market Report of June 2025 spoke of a 12-day Israel-Iran conflict that briefly disrupted the Strait of Hormuz and pushed Brent above $90. It described the situation as a “significant geopolitical risk to oil supply security”. The larger disruption followed on February 28, 2026. The IEA’s April 2026 report recorded that Hormuz tanker loadings fell from more than 20 million barrels per day to approximately 3.8 million within six weeks. Dated Brent reached $144 before declining.The Central Government announced an excise cut on March 27, 2026, reducing the Special Additional Excise Duty on petrol from Rs 13 to Rs 3 a litre and effectively eliminating the corresponding duty on diesel.Speaking at the CII Business Summit on May 12, petroleum minister Hardeep Singh Puri said oil marketing companies were incurring losses of around Rs 1,000 crore per day and added that such a situation was “not sustainable in the long run”.After petrol and diesel prices were increased by Rs 3 per litre, the losses on LPG, petrol and diesel moderated. Sujata Sharma, Joint Secretary in the Union Petroleum Ministry, said during a bi-weekly inter-ministerial briefing on the Middle East situation that the combined losses of oil marketing companies had come down by around Rs 250 crore a day to Rs 750 crore daily. Government officials also said several countries had increased petrol and diesel prices by 20-80 per cent during the period.The PPAC also revised its Indian basket crude formula around the same period, raising Brent’s weight from 24.5 per cent to 61 per cent to reflect the changed sourcing mix.

What governments should be doing: The IMF framework

The International Monetary Fund (IMF), in a blog post titled ‘Responding to the Energy and Food Price Shock: Getting the Policy Details Right’ has argued that the challenge is not simply whether to intervene, but how to respond without creating larger economic distortions. In a recent note on responding to energy and food-price shocks, the IMF said there is “no one-size-fits-all response”, noting that countries differ in energy dependence, fiscal space, market structures and social protection systems.

Progression of fiscal policy measures for a well-sequenced, incremental response

The global institution described energy crises as a “standard negative supply shock” that simultaneously pushes prices higher, weakens economic activity and creates challenges for policymakers. It said fiscal interventions can play a role, but should be “temporary, targeted, timely, and tailored”.According to the IMF, governments should generally allow domestic energy prices to reflect international costs rather than relying heavily on broad controls. “Price signals play a major role in allocating scarce resources, encouraging efficient use, and preventing shortages,” it said.For households, the IMF said protecting vulnerable groups remains critical because lower-income families typically spend a larger share of their income on food and energy. It said “targeted cash transfers, ideally delivered through existing social assistance systems, are generally the best way” to provide support while limiting fiscal pressures.For businesses, the IMF suggested that support should focus on short-term liquidity issues rather than broader market interventions. Measures such as government-backed loans, credit lines and temporary tax deferrals were described as more effective and easier to reverse than direct grants or equity support.The IMF also cautioned against prolonged use of broad subsidies and price caps, warning that such tools can weaken market signals and create lasting fiscal pressures. “As a rule, full price freezes should be avoided,” it said.The wider economic significance of oil prices extends beyond fuel prices alone. Sustained movements in crude prices can influence trade balances, the rupee and current account trends, linking energy markets closely with broader economic stability. Over time, governments have sought to balance these pressures through measures aimed at moderating inflation risks, ensuring fuel availability and cushioning consumers from sharp disruptions while maintaining economic momentum.